“Lycra bike shorts that take our pulse, count our steps and read our moods are pretty nifty, but they aren’t the change we need.” – Robert Wachter, The Digital Doctor

Information and Communication Technologies (ICT) – ranging from hospital information systems to cloud computing, artificial intelligence, and big data analytics – are rapidly transforming the healthcare sector. The McKinsey Global Institute’s Industry Digitisation Index 2015 data shows that healthcare has traditionally been one of the least digitised sectors globally.¹ Health technologies are now connecting doctors to patients seamlessly, aiding providers with their clinical decision- making and empowering patients to self-manage their ailments. These global innovations are driving rapid growth in the uptake of digital solutions in the Indian health ecosystem against the backdrop of local structural changes such as growing broadband connectivity and increased awareness about health and wellness among individuals. However, we believe that extant health technology solutions need much more contextualisation. This requires that health technology developers understand the stakeholders and second, that the government provides a strong and clear regulatory environment to support the digital health ecosystem in India.

The Ailing Indian Healthcare System

India stood at 145th out of 195 countries on the Healthcare Access and Quality Index, behind Bangladesh, Sri Lanka and Bhutan (Lancet 2018). India’s abysmal performance is also reflected in its health indicators on which it lags behind its peers. The maternal mortality rate at 174 per 100,000 live births is almost seven times higher than that of China (World Bank 2016).

Structural quagmires further exacerbate the problems. The low penetration of the organised payer market puts immense financial pressure on the already cash-constrained population base in India. Healthcare expenditures push 39 million additional people into poverty every year (Balarajan and Subramanian 2011).

With 0.7 qualified doctors per 1000 population, India also faces a shortage of physicians. That ratio is substantially lower than other low- or middle-income countries, according to a 2015 SwissRe study. Consequently, patients often resort to the informal healthcare system for their clinical needs. In addition, Indian healthcare provider space is extremely heterogeneous in terms of clinical knowledge, attitude and practice. Healthcare institutions vary from large hospital chains across Tier 1 cities to single physician clinics in remote parts. Many practising physicians in India are trained only in traditional Indian systems of medicine – Ayurveda, Yoga and Naturopathy, Unani, Siddha and Homoeopathy (AYUSH) – and are unqualified by global standards.

The Healing Touch of Technology

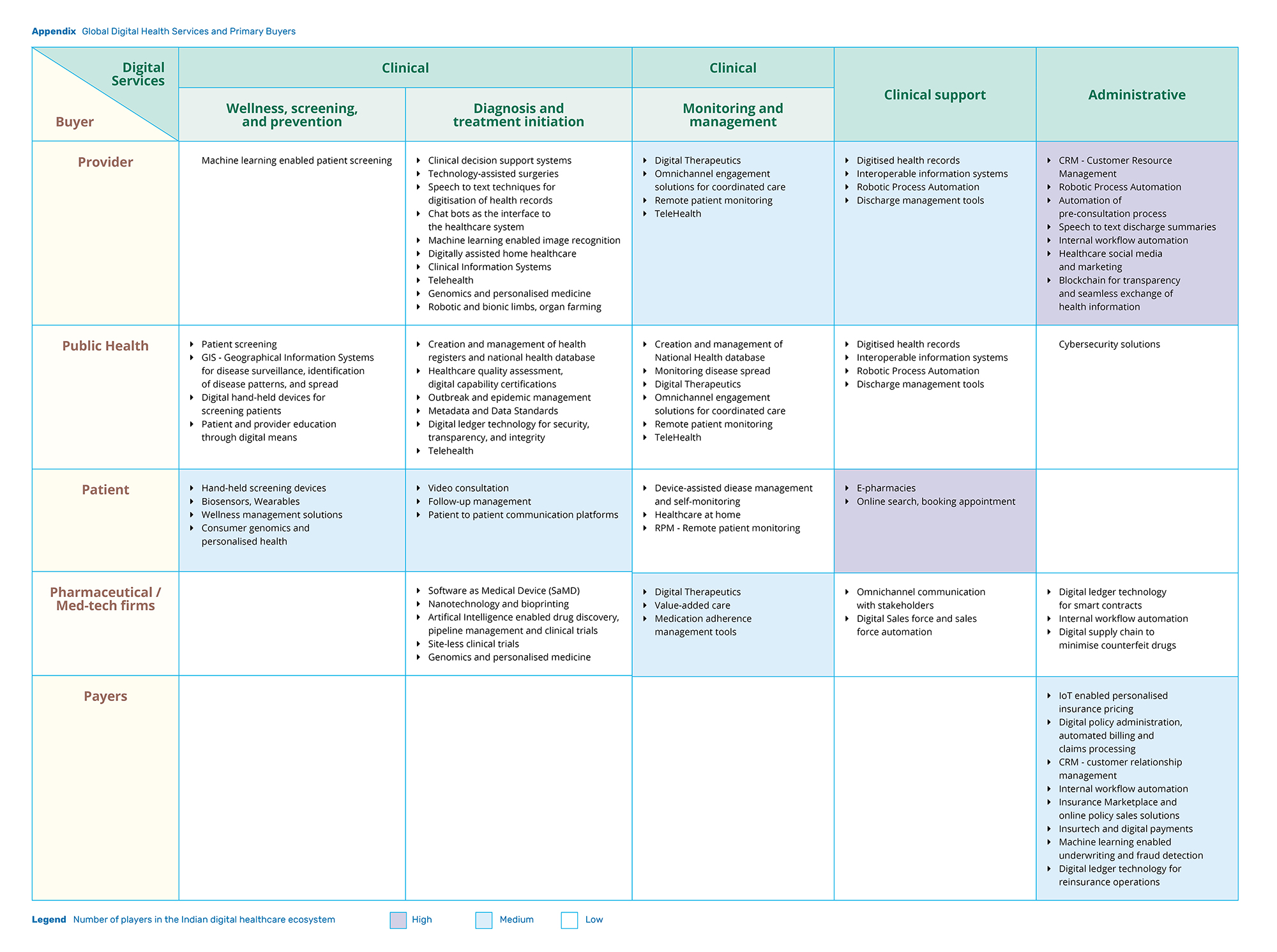

While ICT solutions are often touted as a panacea to all our healthcare problems, a closer look reveals a much more nuanced picture regarding who is using these tools and for what purposes. Stakeholders are consuming technology-led health solutions for a variety of purposes, depending on their varying levels of readiness to adopt ICT (See Appendix: Global Digital Health Services and Primary Buyers). For instance, while providers are mainly using digital solutions for workflow automation and digitisation of health records, patients are leveraging technology to be better informed about their health problems.

Providers – Towards efficient care

Corporate hospital chains lead the way in the use of digital healthcare. However, they vary widely in the extent to which they use available digital features in everyday practices (Powell 2018). Hospitals at the forefront are deploying advanced solutions in pursuit of better clinical outcomes and improved care delivery. For example, digital solutions such as clinical decision support systems provide automated suggestions based on disease condition, medication history and other contextually relevant information from the patient. Consequently, they minimise clinical errors. In contrast, small hospitals and single provider practices have not moved beyond rudimentary ICT solutions like invoice and billing systems.

In rare instances, we see technology being used to develop novel models of care delivery. Aravind Eye Care, for instance, operates primary telemedicine centres called Vision Centres (VCs). Affiliated to a base hospital, each VC is equipped with instruments like refraction cubicles, optical dispensing unit and a computer with a webcam to interact with the base hospital. VCs are only staffed with paramedical staff known as mid-level ophthalmic personnel who can deliver services like preliminary eye examinations, refraction tests and eye-care counselling. Patients who require procedural interventions like surgery or laser treatment are referred to the base hospitals. Aravind Eye Care enhanced the eye-care service reach from 7% to 80% within the first four years of establishment (Shaw and Hathiari 2013). Today, they operate more than 65 VCs, examining an average of 1,800 patients daily (Thomas 2018).

Patients – Consumerisation of healthcare

Technology has the potential to empower patients and make them more active participants in the health system. The most elementary way in which this is happening is by enabling patients to manage diagnostic results online, book appointments and search for provider information on aggregator websites, like Practo, based on reviews and ratings. A few early adopters are beginning to use mobile applications combined with personal health monitoring devices to manage chronic diseases and stay healthy.

Digital solutions such as clinical decision support systems provide automated suggestions based on disease condition, medication history and other contextually relevant information from the patient.

An unusual occurrence in the Indian healthcare ecosystem is that non-healthcare players are tapping into ‘consumerisation’ of health to join the digital health party. For example, leading telecommunications operator Reliance launched JioHealthClub – an inbuilt health app for Jio users. JioHealthClub plans to leverage its subscriber base and collect patient-level clinically-relevant data through hand-held devices. Such platforms and services will enable patients to become comfortable with digital health technologies.

Payers –insurtech on the rise

Only 30% of the total population enjoyed health insurance policy coverage during 2015-16.² However, a few insurance start-ups are leveraging ICT to design innovative products and increase penetration.

Health insurance in India conventionally does not provide coverage for outpatient visits despite the fact that they impose a bigger burden on out-of-pocket expenses when compared to inpatient care (Garg and Karan 2009). The biggest impediment to insuring outpatient visits in India is the ease of fraud. Since most outpatient visits do not involve formal billing, it is easy to furnish fake bills for outpatient consultations and drugs. However, InsurTech is trying to solve this problem. As an example, Max Bupa launched its everyday use digital insurance plan in partnership with Practo and 1mg.

Customers could potentially make cashless transactions for outpatient visits to providers on Practo’s network and fill their prescriptions from online pharmacies such as 1mg. Incumbents too are investing in digital insurance solutions to capitalise on consumerisation of health. Aditya Birla Health Insurance, for example, recently launched an ‘Activ Health’ app which monitors physical activity of policyholders and incentivises them for their healthy lifestyles. The monetary rewards could go up to 2.5% premium value per month or 30% of the annual premium (Gupta 2017). A tech-driven approach could allow insurance firms to assess patient-level risk, promote proactive health, and offer personalised solutions.

The Digital Intervention for India

While recent activity among the Indian digital health stakeholders is exciting to note, there is a long way to go before it has a lasting impact on health outcomes in the country. This journey will require coordinated and concerted efforts from all stakeholders in the health ecosystem. First, the government needs to build a comprehensive regulatory framework that serves the dual objective of protecting patients’ interests while simultaneously supporting digital health providers. Second, the health-tech developers need to design digital solutions which effectively address problems faced by our healthcare system. And last, these digital interventions need to be accompanied by a perceptible business case so that they achieve the necessary scale to make a sizeable impact.

Building an inclusive regulatory framework

The Government of India is recognising the need to regulate digital health. They have embarked upon several initiatives which are intended to reduce the trust deficit between patients and providers in India. First, the central government recently proposed the first draft of the Digital Information Security in Healthcare Act (DISHA) to design the ownership and privacy framework for digital health data. Second, the government appointed the Srikrishna Committee to propose a data protection bill for addressing issues around data transfer, portability, and informed consent. Third, the Ministry of Health and Family Welfare (MoHFW) announced the creation of an online platform for standard Electronic Health Records (EHR) called the Integrated Healthcare Information Platform (IHIP). In addition, NITI Aayog recently proposed the creation of the National Health Stack (NHS) which will make personal health records accessible to beneficiaries based on patient consent.

Initiatives like IHIP and NHS are encouraging first steps. However, their success hinges on private sector participation, since most patients in India get treated in the private healthcare setting. Historically, government schemes have seen a lukewarm response from the private sector. Unaligned incentives, scepticism around commercial viability or an unclear implementation plan could deter private sector participation. The government will need to provide incentives to private players to contribute to the health database.

While DISHA intends to address data ownership and privacy issues, the trust deficit between patients and providers is also driven by the information asymmetry around the quality of care. The first step towards regulating the quality of digital health providers is to expand the regulatory framework to recognise them. The magnitude of this problem is much larger than it seems as the existing Clinical Establishment Act itself is archaic and not implemented in many states. Regulatory recognition of digital health providers will bring in much-needed clarity and allay trust concerns.

Designing the right interventions

Health-tech developers must understand the existing care delivery system to design the right digital health interventions. They need to be mindful of the environment in which the end-user operates. For example, it might not be the best approach to design real-time or synchronous solutions for digital products meant to be used in the remote areas. Designing digital solutions for ‘lite’ or offline usage would be more effective, given the constraints on network bandwidth in rural areas.

Appreciating the user environment is crucial even in urban areas. For instance, the average time spent by an urban Indian provider with a patient is significantly lesser when compared to developed markets. The proposed EHR solutions need to take these time constraints into account. Creative solutions which predict prescription pattern based on patient history and provider practices could reduce the administrative burden of filling out the EHR forms.

Historically, government schemes have seen a lukewarm response from the private sector. Unaligned incentives, scepticism around commercial viability or an unclear implementation plan could deter private sector participation.

Designing the right digital interventions is often challenging because of the digital divide between the user and the technology developers who are typically more adept at using technology than the user. Although the digital divide is a well-recognised issue, it gets further compounded in the healthcare context. Given the disparity of our healthcare system, the haves and the have-nots access very different versions of healthcare systems. This could lead to the digital-haves being impervious to the healthcare problems faced by the have-nots.

Early examples are demonstrating that this divide can be bridged. For instance, Khushi Baby is a combination of wearable tech, mobile-based application and cloud computing to bridge the immunisation gap in the developing world. A newborn wears a pendant with a chip that is loaded with medical histories – such as immunisation schedules, body vitals and more – by a Frontline Health Worker (FHW) using Near Field Communication technology and a mobile application. FHWs need not be connected to the internet while interfacing with patients and the data could be later synced with the cloud when connectivity is better.

Scaling up health-tech efforts

Scaling up health-tech efforts would require a diligent review of challenges. These could be different in the public and private sectors. Most digital health initiatives in the public sector do not get scaled up despite successful pilots. For example, the Indian government launched the Auxiliary Nurse Midwives Online (ANMOL) application in April 2016 after a successful pilot. Designed to assist the Auxiliary Nurse Midwives (ANMs) in identifying and managing beneficiaries of the governmental maternal health programs, ANMOL has seen a weak and fragmented uptake after more than two years of its launch. Many projects suffer from budgetary issues, and others get stuck between the bureaucracy of the state and the central government. Scaling up pilot programmes will require stronger political will and closer coordination between state and central governments.

Digital health scale-up within the private sector is contingent on commercial viability. Among other impediments to digital uptake, the business case for using health technology is often obscure for the providers. This challenge could be overcome by giving incentives to providers to use ICT. For instance, the mandate for private providers to notify tuberculosis (TB) cases to the central database Nikshay had initially seen a lukewarm response. Private providers were sceptical about losing potential revenue once a TB patient was notified and got referred to public facilities. In 2017, the Central TB Division of the Indian government announced monetary incentives to encourage TB case notification among private providers. This is expected to assuage the provider’s concern on notional revenue loss and encourage them to use technology to notify TB cases. Highlighting the benefit – either cost reduction or revenue growth – of using health ICT could be instrumental in digital scale-up among private providers.

Technology: We Reap What We Sow

Technology can fundamentally change the Indian healthcare system. However, technology is subservient to the existing healthcare structure and stakeholder ecosystem. Slapdash applications of health technology without studying the market and end-user could aggravate systemic inefficiencies.

In the worst case, it will lead to technology taking the blame for alien designs and inadequate planning. Lest we throw the baby out with the bath water, we need a conscious effort to identify the right problems and build tailored digital solutions to address endemic health issues. Empathetic design of technological solutions will help us channel the technology juggernaut towards improved health.

Endnotes

¹ Reported in Agarwal et al. (2016).

² IBEF, 2018. Insurance Sector in India: Industry Overview, Market Size & Trends. Retrieved July 27, 2018: https://www.ibef.org/industry/insurance-sector-india.aspx

Know More

Agarwal, R., Chandrasekaran, S. and Sridhar, M., 2018. Imagining Construction’s Digital Future. McKinsey & Company. Retrieved July 27, 2018: https://www.mckinsey.com/industries/capital-projects-and-infrastructure/our-insights/imagining-constructions-digital-future

Balarajan, Y., Selvaraj, S. and Subramanian, S.V., 2011. Health care and equity in India. The Lancet, 377 (9764), pp.505-515.

Central TB Division, 2017. National Strategic Plan for Tuberculosis Elimination 2017-2025. Ministry of Health with Family Welfare. Retrieved July 31, 2018: https://tbcindia.gov.in/WriteReadData/NSP%20Draft%2020.02.2017%201.pdf

Fullman, N., Yearwood, J., Abay, S.M., Abbafati, C., Abd-Allah, F., Abdela, J., Abdelalim, A., Abebe, Z., Abebo, T.A., Aboyans, V. and Abraha, H.N., 2018. Measuring Performance on the Healthcare Access and Quality Index for 195 Countries and Territories and Selected Subnational Locations: A Systematic Analysis from the Global Burden of Disease Study 2016. The Lancet, 391(10136), pp.2236-2271.

Garg, C.C. and Karan, A.K., 2008. Reducing Out-of-Pocket Expenditures to Reduce Poverty: A Disaggregated Analysis at Rural-Urban and State Level in India. Health Policy and Planning, 24(2), pp.116-128.

Gupta, S., 2017. Aditya Birla Health Insurance targeting young Indians through its digital strategy. Mint, October 23. IBEF, 2018. Insurance Sector in India: Industry Overview, Market Size and Trends. Retrieved July 27, 2018: https://www.ibef.org/industry/insurance-sector-india.aspx

Powell, A., Tyagi, H. and Ludhar, T., 2018. Digitising Indian Healthcare Records. ISBInsight, August.

Shankar, K.B., 2016. Trivialiszation of Health Care Scenario in Rural India: A Sociological Concern. International Journal of Humanities and Social Science Studies, 2(6), pp. 89-97.

Shaw, S. and Hathiari, N., 2013. Arvind Eye Care System: In Sync with Technology. IIM Ahmedabad IDEA Telecom Centre for Excellence, Ahmedabad.

Thomas, M.P., 2018. Bringing healthcare to rural India through telemedicine. The Week, May 19.

Wachter, R., 2015. The Digital Doctor: Hope, Hype, and Harm at the Dawn of Medicine’s Computer Age. McGraw-Hill Education, New York.

{kind=link}