It has been nearly a decade since I started researching on the internationalisation strategies of Indian companies. This short article is aimed at capturing the key findings/insights from my papers and research that I felt could be useful to a wider audience. My research associate Sruthi Y was of great help in this effort.

The past decade-and-a-half marked the rapid emergence of a number of firms from developing countries as significant players in the global markets and the number of firms from India was second only to those from China. The global players from India were distinctive as they were from both private and public sectors, whereas a majority of the Chinese global companies were state-owned. This phenomenon was intriguing to me as Indian companies were technologically deficient and resource-poor when compared to multinationals from developed countries. Add to this, the number of successful global companies from India in the previous decades was significantly smaller. This triggered my interest to understand the key drivers and strategies of their internationalisation using a comprehensive sample of Indian companies. I have summarised below some of my key findings.

Inward and Outward internationalisation

I find that the origins of internationalisation of many Indian companies began with the opening up of the Indian economy and liberalisation. By internationalisation, we typically mean ‘outward’ exports, outward FDI, etc. But there is also an ‘inward’ internationalisation. Inward internationalisation involves sourcing activities from foreign markets ranging from import of technology, raw materials, spare parts, capital goods, to financial capital in the form of debt or equity, and induction of internationally trained or experienced managers – all of which may be viewed as a mirror image of the outward process. I found during my research that there are strong linkages between inward and outward internationalisation. Indian companies have leveraged inward internationalisation to upgrade their technological, financial and managerial resources so as to be able to offer products or services, which meet the more advanced needs of the international markets.

Inward-outward linkages are particularly important in the context of knowledge-intensive firms and emerging economies such as India, which was under protectionist policy regime for many decades until they were opened up over the past two decades.

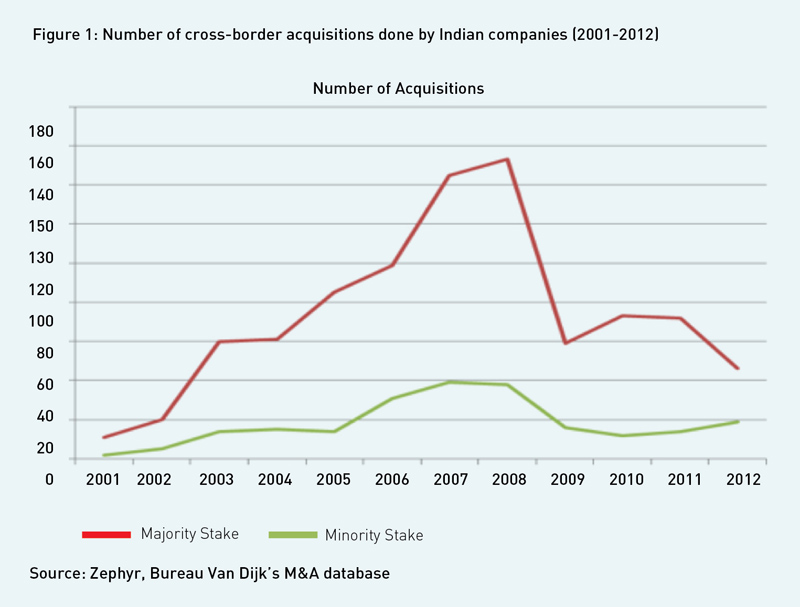

Overseas Acquisitions as the Predominant Mode of internationalisation

Indian multinationals were found to internationalise faster and that too with higher risk entry modes such as via acquisitions compared to other modes. Figure 1 outlines the significant increase in overseas acquisitions by Indian companies during 2001-2012.

Firms could undertake acquisitions overseas for four broad reasons . Some acquire overseas companies to penetrate new markets or maintain existing ones (market-seeking motivation). Another motivation could be – driven by factors of production, primarily natural resources (resource seeking). The third broad rationale is to enhance efficiency, where companies make investments aimed at increasing efficiency (efficiency seeking behavior). Firms can also make overseas investments to acquire knowledge assets such as brands, patents and relationships with clients, etc. (asset seeking behavior). While each acquisition will have some component of all these four, I found that acquisitions by Indian companies are predominantly driven by asset seeking motivations. In other words, Indian companies have used the overseas acquisition route to move up the value chain by acquiring tangible and intangible assets in a much shorter time than what it takes to build them in-house.

Inward-outward linkages are particularly important in the context of knowledge-intensive firms and emerging economies such as India, which was under protectionist policy regime for many decades until they were opened up over the past two decades.

But this strategy is a double-edged sword and has its pitfalls. There are examples of many Indian acquisitions that have lost significant value such as the Betapharm acquisition by Dr. Reddy’s Labs and the Corus acquisition by the Tata Steel.

Affiliation to Business Groups

Business groups (such as Chaebols of Korea or Grupos in Latin America or the Tata group and the Godrej group in India) are a unique characteristic of many economies. A number of studies have investigated whether firms that belong to business groups perform better or worse compared to stand-alone firms and the results have been mixed. Business groups have been found to confer both benefits and costs on the firms affiliated to them. In a number of my studies, I found how affiliation to business groups affects the internationalisation of Indian companies, whether it is through exports or outward FDI, including green field ventures or overseas acquisitions. I found a consistently positive effect of business group affiliation on outward internationalisation.

In other words, business groups confer some advantages which help it’s firms internationalise better. The following are some of the advantages. Resources that are relatively in short supply in developing economies, especially technological and financial resources, are more easily accessible to BG affiliated firms. Firms affiliated to business groups benefit from access to group resources including capital, technology, human resources and complementary products and services and hence are better placed than independent firms in terms of their resource needs. Group-affiliated firms are in a position to leverage linkages with other companies within the group to attain technological partners, suppliers, and other intermediaries to access inputs. Business groups can thus be viewed as an extensive network providing member firms with access to information, knowledge, resources, markets, and technologies. Stand-alone firms need to make additional efforts to form such networks to access the knowledge and resources need for internationalisation.

Role of Owner-CEOs

Firms owned and controlled by business families (as against widely held firms) constitute a majority of the firm population in emerging economies such as India. Also a majority of these family firms in India are headed and managed by members of the owner family (the “owner-managers”). Over sixty percent of the Indian companies in BSE-500 index have CEOs who are also members of the promoter/owner families. These owner managers can play a key role in ensuring their firm’s rapid internationalisation, and their role can probably be even more crucial in situations where the firm internationalises through overseas acquisitions. Compared to other internationalisation modes such as licensing, exports, joint ventures or greenfield projects, foreign direct investments through overseas acquisitions is considered a high involvement and high risk mode of internationalisation. Overseas acquisitions constitute a high risk strategic decision that requires approval and buy-in of all the shareholders. Having the owner (or one of the owners) also acting as the CEO seems to facilitate finalising such strategic decisions better. In one of my studies, I analysed the M&A activities of the Indian companies in the BSE-500 index and found that these companies had executed a total of at least 372 overseas acquisitions between 2002 and 2012. Out of these 372 acquisitions, firms that had the owners also acting as CEOs accounted for a predominant chunk (244 acquisitions or rather 65 percent of the total).

Despite severe constraints and a lower position on the scale of economic development, developing economies can throw up a few companies that are globally competitive and are capable of posing stiff competition to the established multinationals from the developed economies.

Conclusion

Overall the findings of my research on Indian multinationals indicate that, despite severe constraints and a lower position on the scale of economic development, few companies can emerge to be globally competitive and can pose stiff competition to the established multinationals from the developed economies. Armed with superior dynamic capabilities, these emerging multinationals may adopt various strategies such as overseas acquisitions, import of know-how, equipment, financial capital and so on, taking advantage of increasingly liberalised economies and may catch up with the established MNCs sooner than later.

REFERENCES

1 Dunning, John H. “Location and the multinational enterprise: a neglected factor?” Journal of international business studies (1998): 45-66.