The Swiss economy, very much like the Indian economy is shaped by companies, large MNCs and SMEs, which owe their existence, and often their present strength, to their founding families. Examples are the Rieter and Sulzer families, who laid the foundation for today’s large companies by the same names. Further instances of Swiss family entrepreneurship are Novartis (the Sandoz/ Landolt families), Roche (the Hoffmann/ Oeri families) and, last but not least, Holcim (the Schmidheiny family). Decades after the founding of these companies, the familie had to re-invest most of their income in their businesses. However, over time, stemming from constant fl ows of dividends and disinvestments such as taking their companies public, the families have built up and diversifi ed their wealth. Disposition of entire companies have left persons like Ernesto Bertarelli (heir of the founder of the Biotech company Serono, now one of the richest Swiss) with sudden, large, freely disposable funds, that need to be placed and invested.

Indian parallels to the ‘old’ Swiss entrepreneurial families are for example, the Tatas, the Mahindras, Neotias and Sekhsarias. However, many of the ‘younger’ Indian business families who have set up their companies in the recent years of India’s great economic boom will still be in the phase of constant re-investment in their businesses. The constant growth of the businesses, their opening-up to outside investors and IPOs, indicate that these families are in the course of accumulating substantial wealth which will also need professional and customised wealth management sooner rather than later. The accumulation of freely disposable funds (i.e. funds that are not bound in the family business) lead families to look for the best set-up for the management of their family wealth. There are a number of possible set-ups for the management of a family’s wealth. Early stage wealth management is often done by the family itself, or with the help of non family employees of the family business, usually the CFO. Often, the advice of a bank is sought as well. Banks offer financial planning, wealth management and also Family services. Once a very large amount of wealth is accumulated, a lot of families decide to set up their own, independent (non-bank) Family Office.

The key differentiator between an independent non-bank run Family Office and other wealth management services is that Family Offices offer a holistic service which is not restricted to purely the management of financial assets but can cover the entire tangible and intangible “values” of a family. Family Offices provide a long-term oriented service and are set up to manage and serve complex wealth structures. The main differentiator between a bank Family Office and a non bank Family Office is the independence of the latter. Bank Family Offices have to sell the bank’s products and services (at least to a large extent). In addition continuity of professionals (turnover) is a big issue. Bank Family Offices also have to operate in a stringent regulatory environment.

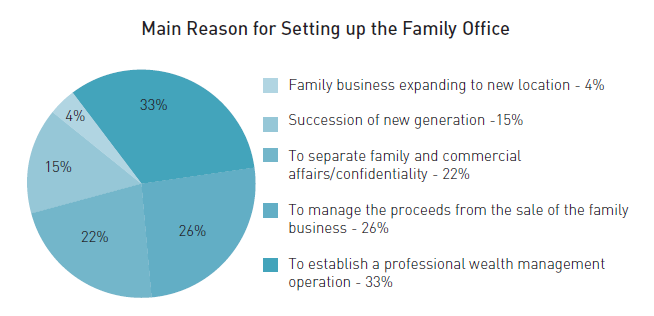

Setting up a cost-effi cient single Family Offi ce, which is able to provide a certain variety and quality of services, requires that the family possesses large investable assets

A Closer look at Independent Family Offices (Non-Bank FO)

The basis for an independent (non-bank) single Family Office is often laid when a business family assigns a well trusted employee, often the CFO/ Head of Accounting, of the family business to take charge of the wealth management and to focus on this task. The traditional “Munimji” of small Indian family businesses, for instance, offered this kind of services. They were loyal employees dedicated to the bookkeeping and cash management of those family businesses. However, as times were changing, the “Munimjis” were lacking the required knowledge and skills of professional asset management. Starting from this nucleus (mostly focusing on financial and tax planning and asset allocation services), the variety and depth of services increased over time. Many full fledged Family Offices offer a whole range of services including legal counselling, philanthropy service, residence management or life management services (e.g. family education, travel service, security etc).

The core task of a Family Office, however, remains the management of the family’s assets. Normally, large wealth features highly complex structures and is segmented in various asset classes including direct investments, traditional investments (stocks, bonds) alternative investments, real estate etc. To handle such a high degree of complexity, i.e. to develop an optimal tax structure and to be able to foresee the development in a multitude of rapidly changing markets, is a highly demanding task that requires the right people and the right process.

Single Family Offices (serving one family only) excel at being independent, securing control and confidentiality and providing a truly individual and tailored service to the family. On the other hand, a single Family Office is expensive and, as a long-term service-provider, there is a certain lack of competition which makes the sustenance of high quality over a long period of time a challenge. “Benchmarking” to best in- class Family Offices is therefore a must, and hiring and retaining the right people with an entrepreneurial mindset is crucial. Setting up a cost-efficient single Family Office, which is able to provide a certain variety and quality of services, requires that the family possesses large investable assets.

Especially in the US, there is a strong tradition and a growing market for independent (non-bank) multi- Family Offi ces which mainly serve clients in the middle segment (e.g. USD 40-250 million)- a job which in Europe traditionally is done by banks, in particular by private banks. US-style Multi-Family Offices are ideal for families which have not too complex asset and/ or family structures. As opposed to bank-affiliated Family Offices, they offer independent service. Multi-Family Offices are cheaper but also lack the 100% control, transparency, and individuality that a single Family Office can offer. Furthermore, with multiple clients a family office always faces various conflicts of interests, such as the allocation of opportunities to their various clients. For a high wealth family with complex structures, it would therefore not be wise to join a Multi-Family Office as the cost factor weighs less important than the disadvantages of the Multi-Family Office model.

However, the Multi-Family Office model deserves some further consideration (for all segments of high wealth), where it is not simply regarded as a means for cost saving but rather as a vehicle for families to form strategic alliances. For example, it could be interesting for a family to join some of the investments of a single Family Office, without any intention to become fully integrated into the Family Office but rather in order to profit from the specific expertise of the single Family Office and the streamlined interests. From the perspective of a single Family Office there is a strong incentive (e.g. share experience, deal sourcing, due diligence) to open up its investment management capacities to other families – nota bene – without becoming a fully-fledged Multi-Family Office, but staying a truly single Family Office with all its advantages.

A recent study by Merrill Lynch and Campden Research among European Single Family Offices has detected certain trends in the development of Family Offices. One is that Family Offices will further strengthen their profile towards being financial service providers – as opposed to life or even lifestyle managers. Another trend is that Family Offices are increasingly including philanthropy services into their service portfolio. Especially the latter could also become true for Indian families which are in the course of setting up their Family Offices. Indian families philanthropy has a very strong tradition, and it deserves to be looked after as well and professionally, as their assets. This is necessary to strengthen the spirit of giving back to the society.

The basis for an independent (non-bank) single Family Offi ce is often laid when a business family assigns a well trusted employee, often the CFO/ Head of Accounting, of the family business to take charge of the wealth management and to focus on this task.

Some Success Factors for Family Offices

The success of a Family Office-measured both by financial performance and the satisfaction of the family with the services provided – is largely built on two aspects: skills and trust. The trust of the family in their Family Office team and a constant flow of information between family and Family Office are the indispensable foundations for successful work. With respect to the right skills, a Family Office must consist of a team of A-class experts who are able to manage a multitude of different assets and in particular, to deal with high complexity and to forecast and react to new mega trends. For example Spectrum Value Management, the Family Office I head, manages over 100 different investments. Our team has to deal with a whole universe of asset classes such as industrial companies, hedge funds and private equity, art collections, real estate and wineries. It has to be knowledgeable about various industry sectors and a variety of geographic regions and countries. Of course, such high complexity cannot be dealt with entirely in-house. To decide what to outsource and to whom to outsource, is a key management task within a Family Office. Not surprisingly, proper tax planning in such a complex set-up is another great challenge. As so often, it is all about people. The recent Merrill Lynch/Campden Research study on European Family Offices has elaborated that retention and motivation of Family Office staff is not all about compensation but also highly linked to the attractiveness of the work itself, job stability and work/life balance. As Family Office staff tends to remain with the same employer over a long period of time, with little internal competition, it is crucial to ensure and demand permanent education so that the knowledge of long-time employees stays up-to date.

Conclusions

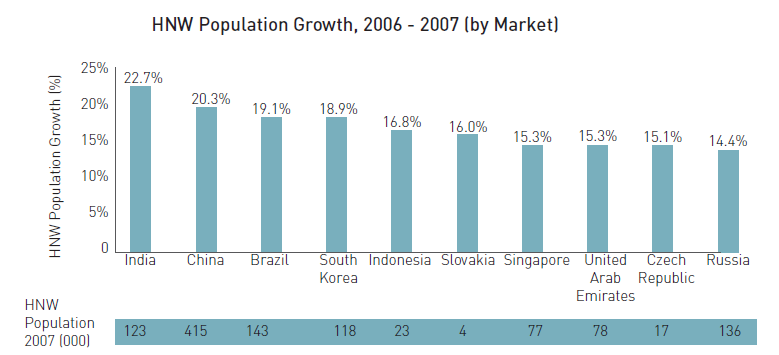

According to the Capgemini World Wealth Report 2008, the High Net Worth Individual (HNWI, defined as individuals who hold at least USD 1 million in financial assets) population of India is growing at 22.7 percent (2007). This means that the demand in India for customised, individual wealth management, in particular, to deal with high complexity and to forecast and react to new mega trends. For example, Spectrum Value Management, the Family Offi ce I head, manages over 100 different investments. Our team has to deal with a whole universe of asset classes such as industrial companies, hedge funds and private equity, art collections, real estate and wineries. It has to be knowledgeable about various industry sectors and a variety of geographic regions and countries. Of course, such high complexity cannot be dealt with entirely in-house. To decide what to outsource and to whom to outsource, is a key management task within a Family Office. Not surprisingly, proper tax planning in such a complex set-up is another great challenge.

The success of a Family Offi ce-measured both by fi nancial performance and the satisfaction of the family with the services provided-is largely built on two aspects: skills and trust.

As so often, it is all about people. The recent Merrill Lynch/Campden Research study on European Family Offices has elaborated that retention and motivation of Family Office staff is not all about compensation but also highly linked to the attractiveness of the work itself, job stability and work/life balance. As Family Office staff tends to remain with the same employer over a long period of time, with little internal competition, it is crucial to ensure and demand permanent education so that the knowledge of long-time employees stays up-to-date. Conclusions According to the Capgemini World Wealth Report 2008, the High Net Worth Individual (HNWI, defined as individuals who hold at least USD 1 million in financial assets) population of India is growing at 22.7 percent (2007). This means that the demand in India for customized, individual wealth management will keep growing alongside a growth in both bank and non-bank Family Office services. Indian business families, who are emerging from the phase of constant re-investing in their businesses, will have to define their needs and decide on the best set-up for their wealth management. For very large wealth a Single Family Office might just be the appropriate solution. In this segment, a Single Family Office is the most effective and the most individualized solution to “play” globalized markets successfully. Wealthy families, with or without their own Family Office, should also consider seeking strategic alliances with Family Offices and profit from their network, expertise, diligence and streamlined interests by joint investing.

The article ‘Family Wealth Management – A European Perspective’ was originally published in the December 2008 issue of ISBInsight. The author, Dr. Dieter Spaelti, has given the below update to reflect relevant information.

In my ISBInsight article ‘Family Wealth Management – A European Perspective’ from December 2008, I elaborated on the structural setup of family offices. As an update, I would now like to focus on one of the key tasks of family offices, which is to formulate a robust long-term wealth preservation strategy.

A long-term wealth preservation strategy for family offices should take both ‘external’ as well as ‘internal’ factors into account. External factors such as the political environment or technological innovations can have a significant impact on family wealth. For example, disruptive technological changes could threaten the longstanding family business. External factors can hardly be influenced; a long-term wealth-preservation strategy should, therefore, be diversified in order to be as resilient as possible in regard to such events. Internal factors like the required cash flow, cost of living needs of the family or the generational transition should form the basis for a clearly defined mandate, which will finally result in the governance structure of the family office.

A long-term wealth preservation strategy for family offi ces should take both ‘external’ as well as ‘internal’ factors into account.

When it comes to the practical implementation, there are different approaches ranging from a simple 60% equities/40% bonds portfolio, or a more diversifi ed endowment model like the one’s of Harvard and Stanford, up to the highly complex ‘all-weather’ strategy that balances risks stemming from changes in infl ation and growth. While each of these strategies will outperform in a different market environment, they all share one common key ingredient – diversifi cation. The utmost relevance of this concept can be illustrated by looking at returns of different asset classes over the last century. While equities have outperformed other asset classes in most decades across geographies, an investor would have experienced a permanent loss of capital if he would have held all his assets in German equities during the period from 1910 to 1930. While war and hyperinfl ation only occur on very rare occasions, a truly long-term wealth preservation strategy should take all possible outcomes into consideration.