Corporate venture capital is one of the multiple mechanisms available to corporations to help them bring in innovations from outside. In tracing the history of CVC, Siva Sakthiraj Rajamani and Professor S Ramakrishna Velamuri highlight its distinct features vis-à-vis pure financial venture capital, and document the rise in CVC activity in China and India.

Corporate venture capital (CVC) is a distinct subset of the venture capital (VC) industry, wherein a firm invests corporate funds directly in external start-up companies, typically in return for a minority stake. CVCs differ from the broader VC industry in the rationale behind the investments; they do not focus on financial returns alone, but also seek to fulfill strategic objectives. This study aims to understand CVC programmes in India and compares CVC deal activity in India and China.

CVCs and the Current Wave of Investment

Henry Chesbrough (2002) states that a CVC investment is defined by two characteristics: its objective and the degree to which the operations of the investing company and the start-up are linked; the degree of synergy between operations determines the purpose of the CVC investments.

Currently, global CVC investments are said to be in their fourth wave (Dushnitsky, 2012). The first wave can be traced to the mid-1960s when the funding of external ventures and/or employee-initiated new ventures was part of the diversification programmes of corporations. With the collapse of the Initial Public Offer (IPO) market in 1973, the first wave of CVC investments came to an end (Gompers and Lerner, 1998). The second wave commenced in the 1980s when the financial markets were once again favorable for venture capital investment, with technology firms and pharmaceutical companies jumping onto the band wagon (Dushnitsky, 2012). The public market crash in 1987 brought an end to the second wave. The third wave in the 1990s was characterized by increased investments in internet-based startups which also pushed the overall venture capital activity. This period saw a surge in the number of corporate venture capital funds (Dushnitsky, 2012). With the 2000 crisis, the third wave of CVC investments ended.

While the first three waves were concentrated in the Western economies, the fourth wave that started at the turn of the twenty first century has had considerable representation from the emerging economies of China and India.

Over the last decade, research on corporate venture capital has picked up in pace. This is the result of a combination of two factors: first, greater keenness on the part of corporations to complement their internal innovation efforts with CVC as a mechanism for bringing external innovations inside; and second, the availability of databases such as the one run by Global Corporate Venturing specifically focused on CVC activity. During the 1990’s, several corporate funds were established to ride the dot-com boom. Chesbrough’s (2002) work followed the withdrawal of investments by nearly one-third of these funds 12 months after the September 2000 (Venture Economics) dot-com bust. Considering the flux in the CVC space at that time, Chesbrough proposed a framework that could help companies decide whether to enter the CVC space on the basis of the benefits they could realize from their investments.

Building on his earlier works, Gary Dushnitsky (2012) noted that the average longevity of a CVC programme had almost doubled during the previous decade. He interpreted this to be a direct result of change in the innovation strategy of corporations i.e., shifts from focusing on internal R&D to embracing external ideas. This is one of the key findings that suggest a change in the objectives of CVC programmes over the last decade. Lerner (2013) concurs with Dushnitsky’s conclusion and has suggested a checklist to minimise risks of failure for CVC programmes.

Brief on the CVC Market in China and India

With the literature suggesting that there have been changes in CVC programmes in the past 12-13 years, this study focuses on understanding the intricacies of these changes with a specific focus on India. However, before proceeding further, it is worthwhile to understand the present state of the CVC market in both China and India.

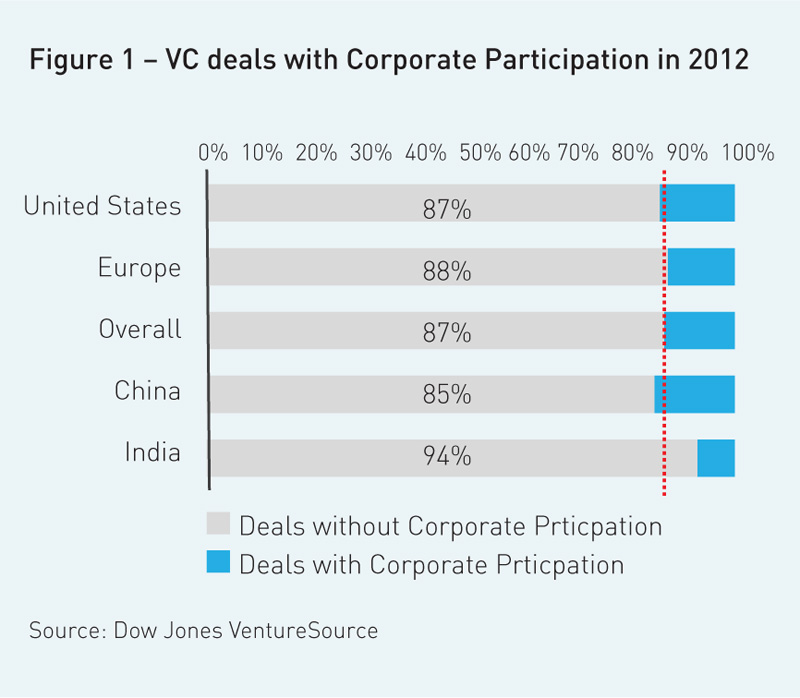

CVC investments represent a healthy proportion of the deals closed overall by VC funds. In 2012, 13% of the equity deals in VC backed companies in the US had corporate participation (Dow Jones VentureSource). The region wise split is provided in the figure below:

China had more deals with corporate participation (15%) than the US in 2012 whereas India had substantially fewer (6%).

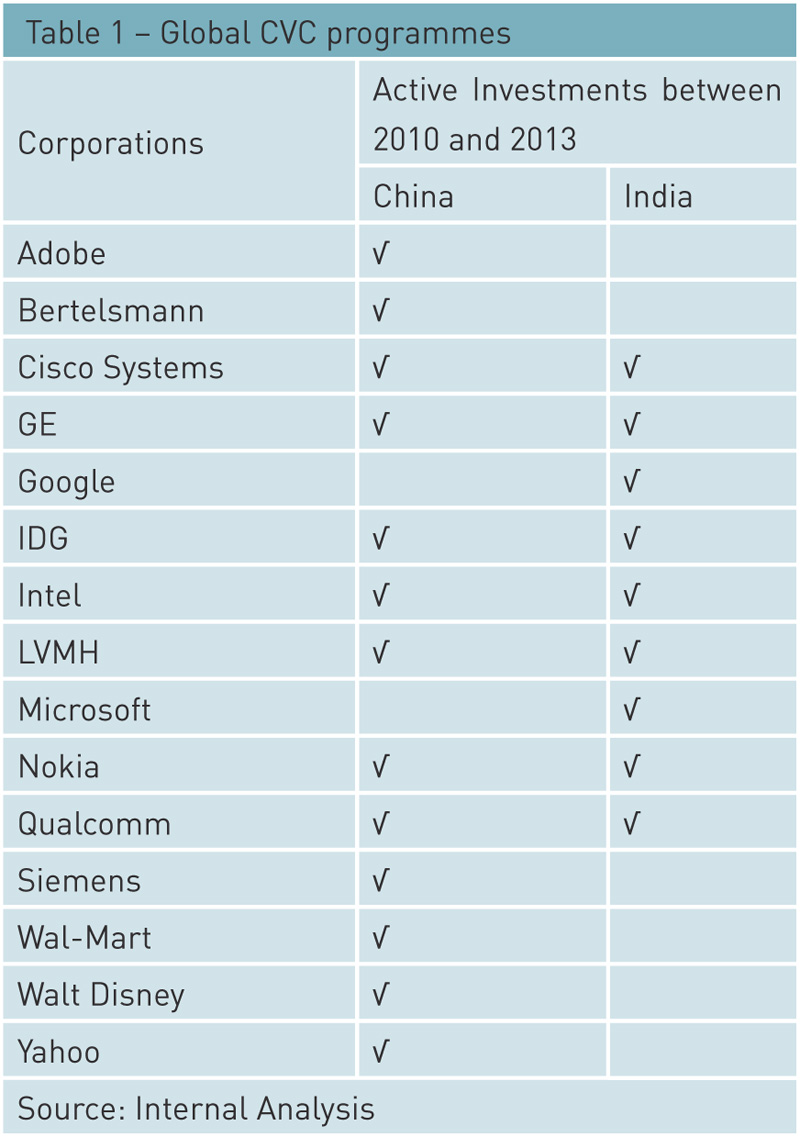

There are several global corporations that have active investing presence in China and India (see Table 1).

Apart from these global corporations, several major local corporations in China and India have an active CVC programme (see Table 2).

According to the Global Corporate Venturing (GCV) database, there were a total of 308 deals (investments) made by CVC programmes in China and India between 2010 and 2013. Of these about 54% of the deals (166) were in China, while the rest (142) were in India (Global Corporate Venturing Database). The yearly deal statistics in China and India between 2010 and 2013 is provided in the figure 2.

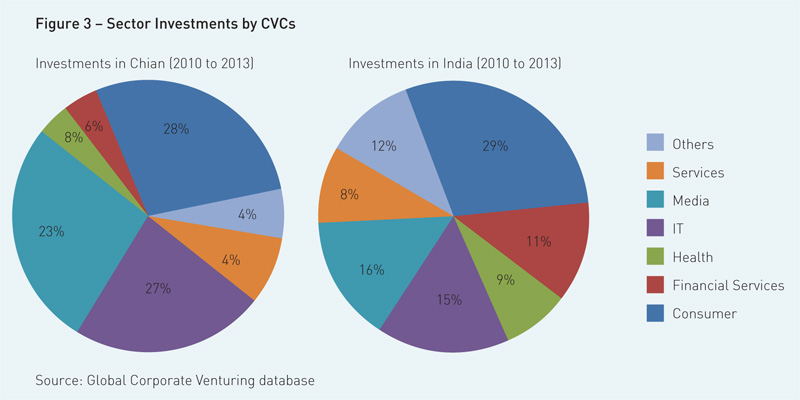

The CVC programmes in these countries have investments across a wide range of sectors (see Figure 3)

The sector investment trends in both countries have followed a strikingly similar pattern, with funds betting on the consumption story in China and India which is reflected in 29% and 28% of investments respectively in the consumer sector. The consumer, IT and media sectors together account for more than three-fourths and about three-fifths of all investments in China and India respectively.

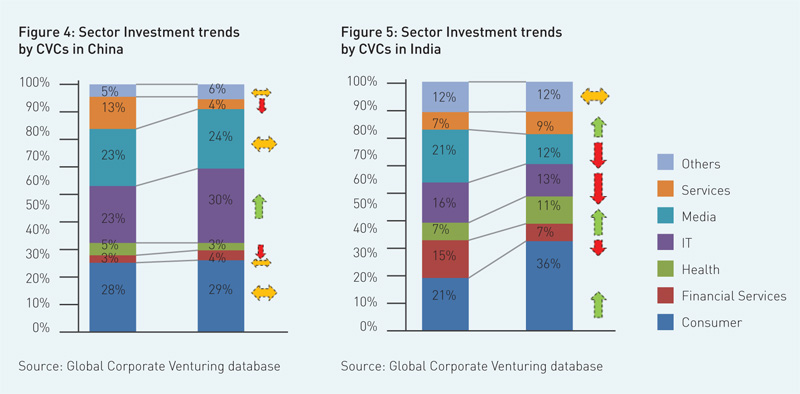

The biggest shift in theme over the last couple of years has been the increase in IT sector investments (see Figure 4). Most of the other sectors have maintained status-quo, with the exception of the services sector, which has shown a substantial reduction in investments.

In India, while the consumer sector has been the area of focus in the last couple of years with more than one-third of the investments targeting this sector, healthcare has also seen substantial increase in interest. The media and financial sectors, however, have seen a considerable decrease in investments.

In terms of deal sizes, we notice a contrast between China and India. While the data are not available for all deals, average deal sizes in China appear to be much higher than that in India. There have been several $20m to $50m deals in China, which are uncommon in India. The sweet spot in India seems to be in the $5m to $10m range. One possible explanation could be that in India, most of the deals seem to be either series-A or series-B funding to the portfolio companies. However, the Chinese market seems to favor later stage deals (series-C and beyond) with consequently higher deal sizes.

Key Findings from the Study

Objectives of the CVC programme

It is important to understand the nature of the strategic objectives of the CVC programmes and their importance.

From our interactions with CVCs in India, a common theme emerges. There is a fine balance between the strategic and financial objectives of the CVC funds. The strategic objectives determine the investment philosophy of most of the funds, while the financial objectives primarily provide the benchmark returns that need to be met.

Financial Objectives

CVCs in India indicated that they had to determine clear financial benchmarks for returns: in some cases, the financial benchmark equaled the returns that would be expected by a purely financially focused VC firm. We did not come across firms that claimed to relax their financial benchmarks in favour of the strategic objectives.

Two explanations could be given for the focus on financial objectives. First, CVC as an investment vehicle has only recently entered the emerging markets. Considering that success stories of VC investments in general in these markets are limited, corporations are choosing to be careful in securing the financial returns on their investments even though the strategic parameters appear strong.

Second, after the 2008 financial crisis, several corporations in emerging markets are facing a credit crunch, which is making corporate leaders uncomfortable with an exclusive focus on strategic objectives. The British Venture Capital Association states that the financial objectives in CVC programmes ‘tend to be used to drive organizational discipline, ensuring that the strategic objectives are met in a manner that ensures the CVC programmes remain sustainable’.

The focus on financial objectives, however, has seemingly affected the risk taking ability in some of the CVC programmes. Purely financially focused VCs are known to take high calculated risks and it only takes one or two investments out of a portfolio of ten to deliver exceptional returns for the profitability of the entire portfolio to be attractive. As a result, VCs are willing to live with high failure rates, where they do not even recover the principal invested.

With CVC programmes being held to stringent financial standards, however, the risk taking ability in some of these programmes seems to have seen a definite curtailing. One of the partners at an Indian CVC programme mentioned that though there is a constant search for ‘elusive returns’, as investors they are wary of investments that fail to return even the capital invested. Therefore, several of the investments made by these CVC programmes seem to be willing to moderate their upside expectations in order to minimize the downside.

Strategic Objectives

Our analysis of the corporate investment programmes in India leads us to conclude that there are some predominant strategic objectives that essentially differentiate them from pure-play VC funds. These strategic objectives typically surface during the investment evaluation stage itself, or in some cases after the investment has been made. The focus of CVC programmes towards investing in those sectors that the parent corporation operates in is itself a good indication of the strategic perspective of these programmes. Only a small minority, more recently, seems to have broadened its horizon and has started to invest in unrelated sectors, although it is rare for them to stray too far from their core areas.

A focus on the sectors that the corporations have an understanding of automatically brings in a strategic perspective. These investments are said to open a window on the latest trends in technology/market to the parent corporation. For corporations operating in sectors high in R&D intensity, such as life sciences or high-tech electronics, etc., this could be looked at as an external R&D department for the corporation. By making investments through CVC programmes, the corporations essentially are addressing gaps left by the internal R&D departments.

Investing in these portfolio companies makes the process efficient for these corporations, from minimising the time required to kick-start similar initiatives in their internal R&D departments to overcoming constraints in the availability of specialised manpower and resources required to carry out these research activities internally. Considering the uncertainty involved in the commercialisation of research, the corporations may choose to bet on some of the programmes in a detached way. The CVC funds provide an excellent platform to be able to do this.

For those corporations that are in sectors without much focus on R&D, a window into what is happening in the market seems to be the primary strategic driver. Making investments through CVC programmes increases the market intelligence of the parent corporation. For example, through its CVC programme a luxury retailer can gain knowledge of customer feedback on niche products by investing in relevant portfolio companies. This gives a preview to the corporation and aids in the subsequent decision making process.

Market penetration came out in our study as the third strategic objective. Typically, some of the investments through CVC programmes are made across the value chain in the sector in which the parent corporation operates. This gives the opportunity for the firm to enhance demand for its product in downstream activities.

The other less common strategic themes suggested by CVC programmes include keeping a tab on what the competitors are doing, and the possibility of entering complementary geographies/businesses in the future.

There is, however, one phenomenon that emerges from our analysis of the strategic objectives of CVC programmes in India that is consistent with global trends. Most of these investments are not made with eventual acquisition of the portfolio company in mind. Though the corporation sometimes keeps an option to acquire the portfolio company, at the initial investment evaluation stage the other strategic objectives that were discussed before are more important.

In fact, in several cases, the possibility to acquire the portfolio company emerges only after the investment has been made and the operations of the company have been observed over a few years.

Investment Process

The deal sourcing is done through standard sources such as bankers and through the networks of the partners/directors at the CVCs. While there may be some inputs from the parent corporation, they are generally limited at the deal sourcing stage.

The inputs of the parent corporation become stronger during the due-diligence stage. Some CVCs interact with the business units at the parent corporation to gain understanding of both the product/service of the company that is under evaluation. There may also be tip-offs about the portfolio company itself if there are some existing relationships. The investment committee makes the final decision and could comprise of representatives from the parent corporation.

Once the investment decision is taken, most CVC programmes follow the standard investment templates followed by VCs. There are investor protection clauses in the investment term sheet such as Right of First Refusal, Right to Pro-Rate etc. These clauses give the CVC programmes and the parent corporation the protection to exercise an option for eventual acquisition of the portfolio company, if required in the future.

While a board seat is generally taken in the portfolio company, there have been some CVC programmes that have chosen not to avail this to avoid governance risks associated with taking board positions in emerging market companies. As an alternative to board seats, some of these CVC funds have taken board-observership positions, also known as quasi-board positions. This arrangement gives the CVCs the required access to information about the company while safeguarding against legal liabilities.

Most of the CVC programmes frequently co-invest with pure-play VCs. This structure has seemed to work to the satisfaction of the partners at CVC programmes.

Post-Investment

Considering that governance is one of the key challenges of startups and growth stage companies in emerging market economies, the CVC funds place emphasis on auditing and company secretary roles for the portfolio companies. The selection of auditors for the portfolio companies is heavily influenced by the CVC programmes in China and India. Further, standard metrics such as cash flow are generally required to be reported to the CVCs by the portfolio companies. However, CVCs are more lenient post-investment in their financial return expectations when compared to pure-play VCs. A CEO of a portfolio company, which has received investment from both a CVC programme and a pure-play VC indicated that when it comes to financial returns, the CVCs have a better understanding of ‘what it takes to take a product to the market’ and hence are willing to stick with the entrepreneur/portfolio company even if there is a time lag in achieving milestones.

There may be interaction between the portfolio companies and business units of the parent corporation after the investment. The CVC funds play a role in facilitating this interaction. However, in most cases they do not voluntarily initiate the dialogue. The request for the interaction has to come from either the parent corporation or the portfolio company.

Hence, while there may be some cross-learning taking place as a result of these investments, in most cases it is just a by-product and not one of the core objectives of making investments through CVC programmes.

Conclusion and Way Forward

Corporate venture capital (CVC) investing has now matured, with considerable action taking place in the emerging markets as well. The objectives of CVC programmes incorporate a strategic dimension – window on technology/product, externalising R&D initiatives, and enhancing product demand are some of the key objectives cited. However, CVC programmes in India have clear financial targets as well that may make or break any investment decision. Hence, there is a fine balance observed between the strategic and financial objectives that drive any investment made by the CVC programme.

Professionals with financial backgrounds outweigh those with operational backgrounds in the Indian CVC programmes that we have studied presumably to ensure financial discipline.

The evaluation of CVC programmes in India has revealed sophisticated mechanisms to achieve strategic and financial objectives for the corporation. With the increased deal activity and robust databases available, further studies could focus on similarities/differences in the structuring of CVC programmes across geographies and industries.

Data Sources: The CVC deal analysis was based on the Global Corporate Venturing database. The qualitative insights are based on 17 interviews conducted – 12 CVC investors with experience in China and/or India, and 5 portfolio companies.

REFERENCES

Chesbrough, HW (2002), “Making sense of corporate venture capital.” Harvard Business Review 80.3: 90-99.

Dow Jones VentureSource, Available at http://www.venturesource.com http://www.venturexpert.com (Accessed on May 12, 2014).

Dushnitsky, Gary (2012), “Corporate Venture Capital in the Twenty-First Century: an Integral Part of Firms’ Innovation Toolkit” The Oxford Handbook of Venture Capital

Global Corporate Venturing Database, Available at http://www.globalcorporateventuring.com), (Accessed on May 12, 2014).

Gompers, P and Lerner, J (1998), “The Venture Capital Revolution” American Economic Association. Journal of Economic Perspectives.15 (2001) 2 (Spring): 145-168

Venture Economics, Available at http://www.venturexpert.com (Accessed on May 12, 2014).